Executive summary (for busy pros): Over half of U.S. mortgages carry sub-4% coupons, and a large share of Colorado owners either have no mortgage or hold ultra-low fixed rates. That dynamic has suppressed listings and kept churn below historical norms. As mortgage costs normalize in 2026, the first sellers to re-enter the market will come from predictable segments: the ≥4% mortgage cohort, select investors, and owners facing life-event triggers. This long-form post quantifies Colorado’s stock by mortgage status, isolates which Denver-area sub-markets are most responsive, outlines a pragmatic 2026 prospecting strategy, and shows how to use TimeToSell.AI to surface the exact households most likely to move despite the lock-in effect.

1) The lock-in effect, defined for a Colorado audience

The lock-in effect describes how homeowners with unusually low mortgage rates refrain from listing their homes because moving would require abandoning a cheaper, fixed payment. The phenomenon is strongest when current market rates are materially higher than a homeowner’s existing note. During 2020–2022, hundreds of thousands of Colorado borrowers refinanced or originated mortgages at historically low coupons. The result is a large stock of owners whose monthly payment position is too favorable to surrender lightly.

For transaction professionals, the practical consequences have been:

- Scarcer resale inventory (fewer new listings), especially in popular neighborhoods.

- Slower owner turnover (lower churn) relative to 2015–2019 baselines.

- Segment-dependent elasticity to rate changes: owners at ≥4% respond more readily to lower rates; free-and-clear owners respond more to lifestyle or investment math.

2) Colorado stock by mortgage status: sizing the segments that matter

To align your prospecting with market physics, start with the stock. At a high level, Colorado’s owner base can be framed in three buckets:

| Segment | Primary Move Trigger | Relative Churn Today | Rate-Drop Sensitivity |

|---|---|---|---|

| Free-and-Clear (~30% of owners) |

Life events, portfolio strategy | Low | Low (financing optional) |

| Mortgage <4% (~55% of mortgages) |

Strong life events, equity/lifestyle upgrades | Very low | Low–moderate (payment delta still large) |

| Mortgage ≥4% (~45% of mortgages) |

Cost relief, refi, trade-up, relocation | Moderate | High (first movers as rates ease) |

Why this matters: your pipeline stalls if you target the wrong stock. In a lock-in era, success is about aligning outreach with: (a) owners who must move (life-event pressure), and (b) owners whose financing position improves enough to justify a move.

3) Who moves even with a 3% mortgage? Identifying the exceptions

Many owners with sub-4% loans will continue to hold. The segment that will move anyway shows clear traits:

- Heirs and estate executors: Death of an owner collapses the lock-in advantage. See our guide: "Why Out-of-State Heirs Are Motivated Sellers."

- Divorce and household changes: Life restructuring trumps payment math.

- Job relocation: Mandated returns to office or PCS orders can trigger non-discretionary sales.

- Function mismatch: The need for a ranch-style home, accessible features, or less maintenance. Equity enables a right-size move. See our playbook: "How to Find Trapped Equity Downsizers."

- Capex and insurance shock: A new roof, foundation issues, or soaring HOA dues. A low rate won’t offset a rising total housing cost. See: "How Insurance & HOA Shocks Create Listings."

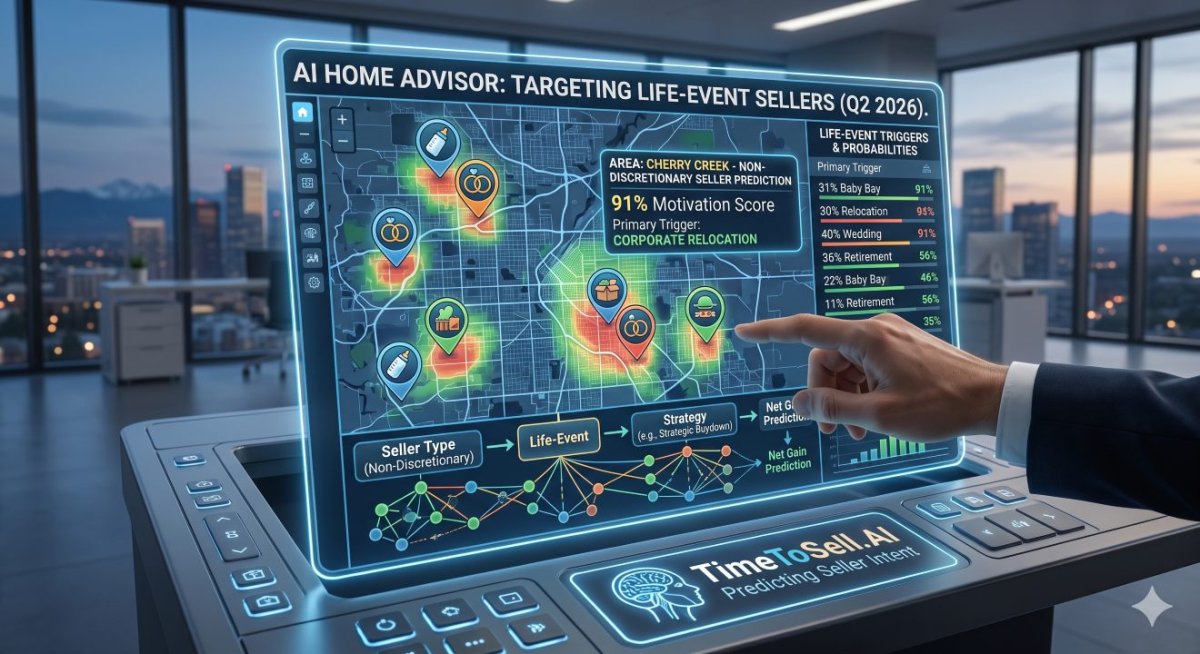

TimeToSell.AI surfaces these owners by cross-referencing ownership length, deed changes, public legal records, lien activity, HOA signals, and local claim/assessment proxies—then scoring move-likelihood at the property level.

4) Prospecting playbook: exact steps for 2026

4.1 Identify and prioritize the right households

Within your farm, rank owners by a blended score:

- Mortgage sensitivity: ≥4% coupon owners first; then sub-4% who show life-event markers.

- Equity position: Strong equity enables list-then-buy, bridge options, and flexibility on concessions.

- Property-type pressure: High dues, assessments, or insurance pushes condo/townhome sellers up the list.

- Tenure & age: 12–20 years in place; approaching retirement; empty nest signals.

TimeToSell.AI automates this ranking and exposes the why behind each score so your outreach is specific, not generic.

4.2 Message frameworks that overcome lock-in fear

For the Sub-4% Owner:

“I understand completely—a 3% rate is an asset. The families I see moving today aren’t focused on the rate they’re leaving, but on the life they’re moving toward. If the current house no longer fits, we can look at how your equity can create a more comfortable monthly payment on the next one, even in this market.”

For the ≥4% Owner:

“As rates begin to normalize this year, you’re in a great position. The payment difference for your next home is much smaller than for others. We can even use seller credits to buy down your new rate, potentially getting you a better monthly payment than you have now.”

5) Pricing and concessions in a normalization cycle

Even as rates ease, 2026 is unlikely to recreate 2021 dynamics. Practical guidance for sellers:

- Price to the active pool: Evaluate live competition, not last spring’s headline.

- Use concessions surgically: Credits and buydowns that target the buyer’s pain (monthly payment) often outperform broad price cuts.

- Stage for functionality: For downsizers, highlight single-level living and low-maintenance features.

6) Related reading

- The Winter Pipeline: Building Your Spring 2026 Listings

- Mastering Micro-Markets in Denver Metro

- 2026 Colorado Housing Outlook

- The HELOC Squeeze: Finding Sellers Trapped by Rising Rates

Next step: put these insights to work in your exact farm. Activate your free TimeToSell.AI account and claim your $100 lead voucher. See which owners in your Denver-area territory are most likely to list as rates normalize—and start the conversation with the right message.